Imposing additional services for MTPL insurance

What to do if additional insurance is imposed on you

Car owners continue to accuse insurance companies of imposing additional services when purchasing compulsory motor liability insurance and complain about the difficulties in purchasing these policies. We'll tell you how to act when unscrupulous insurers avoid selling compulsory motor liability insurance or impose additional services.

Imposing additional insurance to OSAGO in numbers

RSA continues to monitor sales of MTPL contracts on a daily basis. First of all, in those regions where the situation with the implementation of policies is the most difficult. When the Central Bank announced changes in the direction of growth (by an average of 50%) the basic rates of compulsory motor insurance, which began to operate on April 12, in most regions of the Russian Federation a critical situation arose with the availability of these policies.

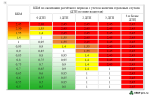

RSA published preliminary results of daily monitoring. Over the five days of April (from 6 to 10) 2015, the union received 235 claims against insurance companies and insurance agents, almost all of them were verbal: motorists contacted by phone or came to the RSA representative office and talked about problems with sales.

Most of the complaints relate to refusals to enter into MTPL contracts and the imposition of other insurance . The largest number of complaints was registered in the Ural Federal District - 118, of which 73 related to refusals to sell compulsory motor insurance, 38 - to the imposition of additional services, 7 - to the remoteness of branches of insurance companies. 12 appeals were accepted in the Far Eastern Federal District, 27 each in the Siberian and Southern Federal Districts, 31 in the Volga Federal District. During the specified period, the executive office of the union received 4 requests for refusal to sell the policy and 16 for the imposition of additional services. But, naturally, not all “victims” complain to the RSA.

How insurers refuse to sell OSAGO

On the eve of the increase in prices, insurers did not want to sell policies at the previous rates and in every possible way prevented consumers from concluding compulsory auto insurance contracts. In addition to customer complaints about long queues at points of sale and reduced working hours in companies, other reasons were added. As before, motorists complained about attempts to “foist” additional services (for example, insurance for an apartment, house, cottage, accident, life, etc.) when purchasing compulsory motor liability insurance. Insurers inform those policyholders who do not agree to additional services that the forms have run out or justify the refusal with some kind of management order. Also, insurers often refuse to sell compulsory motor liability insurance , since allegedly there were technical failures in the AIS RSA database (a unified database on compulsory motor liability insurance), and this is often not true.

Refusal to conclude an MTPL agreement is unlawful!

Nikolai Tyurnikov, who is the president of the gas station, argues that any refusal by the insurer to sell a policy, regardless of the reason, is considered unfounded . OSAGO is a public contract, therefore the insurance company is obliged to conclude such an agreement with each interested client. Car owners who, when trying to purchase an MTPL policy, come across unscrupulous insurers and the imposition of additional services, are usually forced to apply for the desired document to several companies. “This causes indignation among drivers only when they have bypassed a dozen companies - and, accordingly, in this case they begin to act somehow,” says Mr. Tyurnikov.

Cases of lawful refusal in compulsory motor liability insurance

RSA says that it is lawful to refuse to sell compulsory motor liability insurance in a situation where the insurer has run out of policy forms and cannot obtain additional ones because it has exhausted its quota for them. Also, the refusal is considered legal if the consumer has not provided the entire package of necessary documentation or it does not meet the requirements. If the insurance company explains the situation by exhaustion of the quota, the client is recommended to request a reasoned response from it in writing, which must subsequently be sent to the Central Bank or RSA.

What to do if additional insurance is imposed on compulsory motor third party liability insurance

“If an insurance company still does not want to sell compulsory motor liability insurance, this needs to be recorded somehow. You can send an application to the insurance company to conclude an insurance contract in the prescribed form. This is done by mail with acknowledgment of delivery. This will provide an opportunity to prove that the company received your application. The fact of refusal to sell a policy in the office itself can be confirmed using audio, photo or video devices. These means should make it possible to identify the circumstances and location of the failure, as well as determine the exact date and time,” the RSA explains.

How to record a refusal to sell an MTPL policy

Mr. Tyurnikov says that insurers do not give written refusals. Therefore, it is sufficient to record the fact of refusal to sell a policy or the imposition of additional services with witness testimony (in writing with contact information of witnesses) and a video or audio recording. Next, you need to write an application to the Central Bank. “The regulator will not speculate whether there is enough or not enough evidence. There is confirmation - that's it, an instant fine. Therefore, it is better to visit one insurance company with a witness (acquaintance, friend) than to run around many organizations alone, faced with a problem,” he recommends and reminds that for refusal to implement an MTPL policy, the insurer faces sanctions - a fine of 50,000 rubles. “If they refuse a hundred clients, they will accordingly pay a fine of 5,000,000 rubles,” the expert emphasizes.

Be careful when recording photographic and video evidence

Vyacheslav Golenev, a senior lawyer at the Moscow bar association Zheleznikov and Partners, believes that video recording is unacceptable in disputes with insurers, since Article 152.1 of the Civil Code of the Russian Federation states that the publication and subsequent use of a person’s image (including his photo, video recording or work artistic art on which it is depicted) are allowed only with the consent of this person. “This also applies to insurance company employees,” he adds.

What is an imposed service?

Igor Yurgens, head of RSA and VSS, believes that it is often difficult to separate the imposition of services and cross-selling . He considers abuse to be situations in which a mandatory condition for concluding a compulsory motor liability insurance contract becomes the condition of purchasing a policy for another type of insurance or another service. (We must remember that not only another type of insurance can be imposed, but also a technical inspection and even a requirement to wash the car for a couple of thousand.) “If cases of imposition of additional services are confirmed and we receive unbiased complaints, RSA will begin to use tough measures, based on the rules of the professional activities and legal requirements,” the expert warns.

Where to turn if the insurer refuses to sell a compulsory motor liability insurance policy

Oleg Shebanov, who heads the underwriting of motor vehicles at the BIN Insurance company, is confident that the recent increase in basic tariffs under MTPL contracts can only partially solve the problem of motorists, because the April increase in prices for motor vehicle insurance for a number of Russian regions is still insufficient . “We should not forget about the rise in cost of spare parts (this will affect the degree of loss of the product) and the increase in liability limits. An increase in tariffs for many branches will eliminate the problem with the lack of policy forms, but for unprofitable regions it will not solve the problem,” the expert states.

Motorists who encounter difficulties when purchasing compulsory motor insurance have the opportunity to contact the RSA, which receives requests and complaints from policyholders about the actions of companies. The complaint form is available on the RSA website. For any questions, please contact the RSA toll-free number: 8800-2002275, (495) 641-2785 (for Moscow residents).

Imposing life insurance when purchasing compulsory motor liability insurance

Good afternoon, dear reader.

In this article we will talk about imposing life insurance when purchasing an MTPL insurance policy .

In the second half of 2014, many readers of the pddmaster.ru website contacted me, describing approximately the following situation. When contacting an insurance company to purchase an MTPL policy, the driver learns that in addition to the basic cost of the policy, he will have to pay additional life insurance or some other services (about 1,000 rubles).

Note. It must be said that drivers do not encounter the imposition of services every time they contact an insurance company. In some “good” years, all insurers sell MTPL without any problems, and in some “bad” years, insurance agents try with all their might to sell insurance as expensive as possible, or even refuse to sell it at all.

Imposing additional services is illegal (Part 2 of Article 16 of the Consumer Rights Protection Law), but many drivers do not know about this and do not even try to defend their rights.

Let's look at a few ways insurance companies try to sell life insurance. The content of the article:

A few words about the history of the issue. Rumor has it that compulsory motor liability insurance is an unprofitable type of service for many insurance companies. In 2014, the payment limits for compulsory motor liability insurance were increased several times; insurance rates did not increase so significantly. In this regard, some insurers generally refuse to sell MTPL policies, others are trying to impose additional services on car owners that most drivers will never need.

To be honest, the true extent of the situation was difficult to appreciate until I contacted several insurance companies at the end of 2014. The time has come to replace the MTPL policy, and I had the opportunity to talk with several insurers. This article is about insurance companies in the city of Ryazan; perhaps in other cities the situation is more positive.

Note. As a rule, problems with the purchase of compulsory motor liability insurance do not arise in large cities (Moscow, St. Petersburg). You can always buy insurance there and at normal prices.

Difficulties usually arise in remote regions. For example, quite often complaints are received against insurance companies in the Rostov region.

Imposing life insurance in Rosgosstrakh

So, the first insurance company I contacted in 2014 was Rosgosstrakh. In practice, I didn’t care from whom to buy the MTPL policy, but Rosgosstrakh has the largest number of offices in Ryazan, so I decided to go to them.

The imposition of life insurance when purchasing compulsory motor liability insurance in Rosgosstrakh has been put on stream. And their scheme is quite cunning.

First, the documents necessary for registration of compulsory motor liability insurance are taken from the driver, and the registration and calculation of the insurance premium begins. After some time, the total cost of the policies is announced, which is approximately 1,000 rubles higher than the real cost of compulsory motor liability insurance.

After this, drivers behave differently:

- They don't pay attention . Drivers who have not specified the cost of compulsory motor insurance for the next year in advance may not pay attention to the increased cost.

- Agree with the manager . Most drivers, after a short explanation from the manager, agree to purchase a life insurance policy.

- Disagree with the manager . Drivers who are familiar with the legislation refuse to purchase compulsory motor liability insurance, not being satisfied with the explanations.

Let's consider what arguments the Rosgosstrakh manager uses to impose life insurance:

1. The legislation has changed

The phrase sounds: “The legislation has changed, insurance limits have been increased to 400,000 rubles, life insurance has been added.”

Many drivers understand this phrase as follows: “Life insurance has become mandatory, you will have to buy it.” And they buy both policies.

Although in fact the meaning of the phrase is: “Insurance limits have increased. In addition, the insurer, on its own initiative, added another policy to you, which you don’t have to buy.”

So if the driver doesn’t know whether life insurance is required when purchasing compulsory motor liability insurance, he easily falls for the insurance company’s bait and shells out an additional thousand.

2. Mandatory inspection of the car after 3 months

For drivers who understand that life insurance is being forced on them, there is a more cunning scheme.

The manager explains that at Rosgosstrakh you can buy MTPL without life insurance, but the driver will have to undergo a vehicle inspection. The possibility of conducting an inspection is indeed provided for in clause 1.7 of the Insurance Rules:

1.7. When concluding a compulsory insurance contract, the insurer has the right to inspect the vehicle. The place for inspection of the vehicle is established by agreement of the parties. If no agreement is reached regarding the place of inspection of the vehicle or if a compulsory insurance contract is drawn up in the form of an electronic document, the insurer will not conduct an inspection of the vehicle.

However, the problem is that the waiting list at Rosgosstrakh is approximately 3 months.

Those. in fact, the insurer offers you 2 alternatives :

- For an additional 1000 rubles, buy a policy here and now.

- Drive for 3 months without compulsory motor liability insurance, then get examined and buy a policy.

At the same time, the insurance company will not refuse to conclude a compulsory motor liability insurance agreement. This is quite natural, because the fine for such a refusal is up to 50,000 rubles for an employee and up to 300,000 rubles for an insurance company (Article 15.34.1 of the Administrative Code):

Article 15.34.1. Unreasonable refusal to conclude a public insurance contract or imposition of additional services when concluding a compulsory insurance contract

Unreasonable refusal of an insurance organization, an insurance agent, an insurance broker to enter into public contracts provided for by federal laws on specific types of compulsory insurance, or the imposition of additional services on an insured or a person intending to enter into a compulsory insurance contract that are not stipulated by the requirements of the federal law on a specific type of compulsory insurance -

shall entail the imposition of an administrative fine on officials in the amount of twenty thousand to fifty thousand rubles; for legal entities - from one hundred thousand to three hundred thousand rubles.

To obtain a waiver, drivers are sent to the central office on the other side of the city.

In general, Rosgosstrakh’s scheme is quite cunning, while other insurance companies act more simply.

Imposing life insurance in the VSK insurance house

I didn’t specifically choose the next insurance company, I just went to the first office I came across. It turned out to be the office of the VSK insurance house.

This insurance company also refuses to sell a compulsory motor liability insurance policy without a life insurance policy. Moreover, they don’t have any clever explanations. The manager simply says that he will not sell the policy. Refusal to conclude a contract is also not granted.

If any of the readers have a desire to “fight” with the insurance company, then feel free to go to VSK. Record the refusal on a video camera or voice recorder. After this, you can impose a three-hundred-thousand-dollar fine on the insurance company.

After visiting the second insurance company, it became clear that the imposition of life insurance when purchasing compulsory motor liability insurance has a noticeable scope . Therefore, it was decided to immediately go to the next insurance office with the voice recorder turned on. The office was again chosen at random, but the insurer turned out to be respectable and sold the MTPL policy without any problems.

What to do when imposing life insurance when purchasing compulsory motor liability insurance?

Let's look at what can be done if life insurance is imposed when purchasing compulsory motor liability insurance :

1. Go to a reputable insurance company . As practice has shown, such companies exist, you just need to search a little.

2. “Knock out” the refusal to conclude an MTPL policy . Insurance managers do not issue refusals voluntarily; this will cost them a lot. However, it is possible to force the insurance company to conclude an agreement with you. To do this, you need to write an application and send it to the insurance company by registered mail with a receipt stamp.

The text of the statement should be something like this:

I ask you to conclude an MTPL agreement for a car. and enter the following drivers into it. I am attaching to the application a copy of my passport, a copy of my driver’s license, a copy of the diagnostic card, and a copy of the vehicle registration certificate. Please notify me of your decision by phone and in writing at

The insurer will not be able to ignore a written request. He will either immediately invite you to conclude an agreement or give you a written refusal. A written refusal can be submitted to higher authorities. This will be a very good basis for imposing a fine.

This option makes sense to use only if the insurance company is dear to you for some reason and you do not want to go to another one. Well, or if in your locality all insurers are engaged in imposing life insurance when purchasing compulsory motor liability insurance.

3. Buy life insurance. This option is the simplest, which is why most drivers choose it.

However, I recommend that you first fight at least a little for your rights, go to different insurance companies, and try to get a written refusal. This will be good experience in asserting your own rights, which may be useful to you in the future.

4. Apply for compulsory motor liability insurance via the Internet. The opportunity to buy an insurance policy online appeared in mid-2015. In 2019, all insurance companies are required to sell electronic insurance policies.

Additional services cannot be imposed on the driver via the Internet, so the cost of insurance strictly corresponds to the value calculated using the OSAGO calculator.

Note. Some cunning insurance companies who do not want to sell compulsory motor liability insurance via the Internet imitate technical errors or deliberately delay the document processing process.

However, in 2019, purchasing an electronic MTPL policy is the best option.

Refund of money for life insurance under compulsory motor liability insurance

If none of the “alternative” options listed above suits you, and the insurance company nevertheless imposed additional insurance when purchasing compulsory motor liability insurance, then I recommend that you take up the return of additional insurance.

To do this, you need to contact the insurance company within 5 days from the date of registration of compulsory motor liability insurance.

Please note that the possibility of returning additional insurance must be described in the text of any voluntary insurance agreement. This requirement has been in effect since March 2, 2016, when the Directive of the Central Bank of the Russian Federation “On minimum (standard) requirements for the conditions and procedure for the implementation of certain types of voluntary insurance” came into force.

You need to fill out an application for the return of additional insurance from the insurance company. Usually this procedure goes without problems. If you contact the insurance company within 5 days, you can return the money for the imposed insurance in full.

In conclusion, I would like to note that from the point of view of drivers who follow traffic rules and avoid road accidents, the reluctance to sell insurance looks rather strange. For many years, such drivers simply transfer money to the insurance company (buying MTPL policies) and receive nothing in return. At the same time, the cost of policies is gradually increasing, and for some reason insurers are incurring losses and do not want to enter into MTPL contracts.

Perhaps legislators should introduce amendments that increase the cost of compulsory motor insurance for drivers who regularly get into accidents. It is these drivers who bring losses to insurance companies and troubles to other road users. The high cost of compulsory motor liability insurance for those responsible for road accidents would be a good incentive for careless drivers.

When purchasing compulsory motor liability insurance, they impose additional insurance - what should I do, can I refuse it and how can I return it?

- The insurance company does not have the right to impose additional insurance on compulsory motor liability insurance under the Consumer Rights Protection Law.

- The insurer also cannot refuse to sell a policy without additional insurance, since the MTPL agreement is public.

- The most effective way for 2019 to refuse “additional supplements” is to use the legal cooling period.

- For imposing services not provided for by law, the insurance company, as well as its agents and brokers, can be fined a fairly large amount.

Imposing “additional insurance” in the form of accident insurance, life insurance, items inside the insured car, real estate and others sold together with compulsory motor liability insurance – this has even become a tradition in our country. Insurers are trying to sell everything they can along with the policy, which they say is becoming increasingly unprofitable. But what is the correct way to refuse such “additional provisions” when applying for compulsory motor liability insurance and what to do in this case?

Is it possible to purchase MTPL without additional insurance?

Yes. And here two options are possible for you:

- contact another insurance company where such “extras” are not imposed,

- refuse other products on top of MTPL insurance,

- pay and purchase all additional insurance that is imposed on you, and then return it back to the insurer.

The first option is the simplest and most obvious. But it doesn’t always work for the simple reason that other insurance companies may impose additional things on you that you don’t need, or even more expensive than the first one. In addition, if we are talking about a small town, then another insurance company may be quite far from you.

The second option is not so simple - if you refuse additional insurance, then the policy may not be sold to you for various reasons: either the forms will run out, or the computer will freeze, or the employee’s working day will end (and the next one will never begin), etc. . Yes, the situation began to improve significantly in 2019. Just a few years ago, it was almost impossible to buy a compulsory motor liability insurance policy without additional imposed additional services and products, and if it was possible somewhere, there was a queue for a month or two.

But the third option is the most favorable in terms of the number of visits to various authorities and institutions, including the insurance company.

So, let's talk about everything in order!

The insurance company cannot refuse to sell the policy!

According to Article 1 of the Federal Law on Compulsory Motor Liability Insurance, an insurance contract (in other words, a compulsory motor liability insurance policy) is public. This follows by definition of such a contract. And for public contracts there are serious requirements under Russian legislation. Thus, according to Part 3 of Article 426 of the Civil Code of the Russian Federation, an entrepreneur is prohibited from refusing citizens to enter into a public contract.

All this means that the insurer does not have the right to refuse to sell MTPL insurance to the car owner. But such a right appears if there is no objective possibility of concluding an agreement.

Is the functionality of the computer and the availability of policy forms such an opportunity? Yes it is. Accordingly, otherwise the insurance company has every right to refuse to sell you insurance.

Further - worse

Moreover, a refusal to practically enforce the protection of your rights can only be in writing. To receive it, you need to submit a written application to purchase an MTPL policy.

But there is an important subtlety here - the time for consideration of your application by law is as much as 30 days (Part 1 of Article 445 of the Civil Code of the Russian Federation). This means that if you applied for insurance a day or two or a week before the expiration of the current one, then waiting for a written refusal is not your option, because there will be a period when you simply will not be able to drive a car due to lack of insurance.

Thus, if there are at least 30 days until the end of your current MTPL policy, then when imposing “additional insurance” the best option for you is to submit an application in writing (and take a copy of the application with a stamp of acceptance for video recording), which the insurance company is authorized to consider for 30 days and after that, give a reasoned refusal or enter into an insurance contract.

If the insurance company refuses you illegally and directly “out of lawlessness” - on video or in writing, then below we have instructions on how to attract a large fine for this.

The insurance company has no right to impose “extras”

Everything is very simple! Since an insurance company is an organization or individual entrepreneur (agent or broker for selling policies), you are an individual who is going to buy an insurance service for money, then consumer relations apply between you and, accordingly, the consumer protection law applies.

And, according to Part 2 of Article 16 of the Law on the Protection of Consumer Rights, it is prohibited to condition the purchase of some services on additional services - that is, the purchase of compulsory motor liability insurance with any other insurance, banking services and any other products.

Is it possible to refuse additional insurance and how?

So, we have come to the most important thing - the Central Bank in our case provided the best opportunity to avoid the imposition of additional insurance when purchasing compulsory motor liability insurance in the form of the opportunity to refuse the first ones with minimal damage to yourself (except for allowing you to use your own funds).

We are talking about the so-called cooling period. The cooling-off period is the consumer's opportunity to change his mind and cancel any voluntary insurance within 14 days after purchasing it.

This right for you is contained in the instructions of the Bank of Russia dated No. 3854-U on the requirements for concluding insurance services. According to the very first paragraph of this instruction:

1. When carrying out voluntary insurance, the insurer is obliged to provide a condition for the return of the paid insurance premium to the policyholder in the event of the policyholder’s refusal from the voluntary insurance contract within 14 calendar days from the date of its conclusion in the absence of events in this period that have signs of an insured event.

Until 2018, this period was shorter - 5 days, but then the Central Bank made changes to the cooling period.

As you can see, you can refuse and return all additional insurance within 14 days after purchasing it. Although, to do this, you will still have to first purchase them along with compulsory motor liability insurance. At the same time, according to paragraph 5 of the same instructions, the insurance company is obliged to return the money in full. But paragraph 6 immediately says that the refund amount is calculated in proportion to the validity period of the additional insurance. However, its effect does not necessarily begin the next day after purchase.

There are very rare exceptions when it is impossible to return the imposed “extras”:

- if you are a foreign citizen and are in Russia for work purposes, and additional medical insurance has been imposed on you,

- if during this time there was an insured event under additional insurance and you have already applied for compensation for damage,

- if this “addition” is mandatory for you (provided for by law) when carrying out your professional activities,

- if you were sold an international MTPL.

Return instructions

- First of all, you will have to buy compulsory motor liability insurance along with all the imposed additional insurances - alas, but this cannot be avoided in our case.

- Next, within 14 days, you must submit a free-form application to waive additional insurance with a request for a refund in cash or non-cash form. In the latter case, you need to indicate your account details for crediting.

- The insurer within 10 working days (clause 8 of the Instructions) is obliged to transfer the money to your account or return it in cash at your choice.

Is it possible to hold the insurance company liable for a fine for imposition?

Yes. And the fine for her will be as much as 50 thousand rubles. You can be held liable not only when purchasing a compulsory motor liability insurance policy directly at the office of the insurance company, but also from agents or brokers.

We are talking about a specially created article for this purpose, 15.34.1 of the Administrative Code. It provides:

- a fine on officials of 20-50 thousand rubles for refusing to sell a policy or imposing “additional restrictions” when purchasing compulsory motor liability insurance,

- a fine for the organization of 100-300 thousand rubles for the same actions.

At the same time, agents and brokers are recognized as officials, including if they work as individuals - not individual entrepreneurs or LLCs, but as organizations - directly offices and branches of insurance companies.

But it is important to have evidence of this violation. The best of them is a video recording where the employee’s refusal to sell the MTPL policy without purchasing additional health/medical, real estate, property or accident insurance is visible and heard.

Next, this video must be attached to the application to the prosecutor’s office and submitted to the location of the insurance company’s office.

What to do if they impose additional services on compulsory motor liability insurance or refuse to issue a policy?

Insurance companies can, within certain limits, change the price of compulsory motor liability insurance policies in order to regulate unprofitability. However, even this did not help solve the problem of imposing additional services. At the same time, some insurance companies refuse to issue motor vehicle insurance at all. What can you do to defend your rights?

Evidence base

Even if the car owner has legal grounds to file a complaint against the actions of the insurance company, we must not forget that the fact of the violation still needs to be proven. Yes, sometimes courts and various government agencies are content with oral statements from motorists, but there should be several such citizens.

The car owner cannot know how many citizens’ rights the insurance company violated, therefore, it is better to stock up on evidence in advance. In this case, the client will easily prove the violation of his legal rights, and the insurer’s managers will not be able to avoid punishment. You can use as evidence:

- video recording of the violation;

- written response from the insurer;

- eyewitness testimony.

Friends of the car owner may be brought in as witnesses. If you suspect that problems may arise when applying for a policy, you should invite a couple of friends with you. This is an important point because other visitors to the insurance company's office may be reluctant to testify.

How to deal with the imposition of additional services?

To avoid difficulties when purchasing a compulsory motor liability insurance policy and at the same time not pay for additional insurance services, it is worth purchasing an unnecessary policy. At first glance, such a recommendation looks absurd, but only if the client does not know about the possibility of returning money for the imposed insurance. This can be done within fourteen days from the date of registration of such a policy, but only if the client has not applied for payment under the imposed insurance.

Control over the implementation of this rule by insurers rests with the Central Bank. Actually, the insurance company’s obligation to return money for additional insurance is controlled by this organization. Complaining about violations when returning insurance premiums for imposed insurance should be made to the Central Bank, which has created a separate page on its website about the cooling-off period.

If you still have a strong desire to buy an MTPL policy without overpayment, you should complain about the actions of the insurance company’s managers to the Central Bank.

If there is evidence, the insurer will be required to issue a motor vehicle license without imposing additional services. In addition, the insurance company will face a large fine, as will the manager responsible for imposing voluntary insurance. The car owner can also appeal the actions of the insurance company to the prosecutor's office.

Legal grounds for refusal

As is known, insurance companies licensed for compulsory motor liability insurance do not have the right to refuse clients to issue compulsory motor liability insurance policies. However, we must not forget that the client is also obliged to comply with the requirements of the law, but sometimes car owners or their representatives forget about this obligation. So, the insurance company has every right to refuse insurance in the following cases.

- The car owner's representative does not have a notarized power of attorney for the car (with the right to insure).

- Originals of required documents are missing.

Buy OSAGO online – easy ordering and price comparison

In addition, a car owner may be denied the sale of insurance if there is no connection with the automated PCA database. It should be borne in mind that often insurers simply deceive policyholders. If the manager reports that there is no connection with AIS RSA, but at the same time issues an MTPL policy for another client, the car owner has grounds to appeal the refusal. In this case, he can contact the Central Bank or the prosecutor's office.

When should you complain to your insurer?

Not all car owners are aware of their rights, which managers of some insurance companies tirelessly take advantage of. Sometimes insurer employees outright refuse to issue a client with a compulsory motor liability insurance policy. Of course, such a refusal has no legal basis, so the client has every right to seek help from the Central Bank or the prosecutor’s office.

Also, insurance companies often refuse to issue car title to car owners due to the lack of forms. Sometimes managers actually run out of forms, but more often they are safely hidden, for example, in the office director's safe. If there are any doubts about the honesty of the insurance company’s employees, the car owner needs to complain to one of the previously mentioned authorities.

When filing a complaint, the car owner must understand that resolving the issue may take a long time.

If the insurance period is about to expire or has already expired, the policyholder will actually be deprived of the opportunity to use the car. In Russia, it is prohibited to operate a car without a valid MTPL policy; for such an offense, the motorist faces a fine. In addition, in the event of an accident, he will have to independently compensate for the damage caused.

To avoid negative consequences, after filing a complaint, you should worry about finding a more adequate company. This will allow not only to punish the insurer who violated the law, but also to promptly renew the MTPL policy and continue to use the car.

Alternative option

If the owner of a car wants to eliminate any difficulties when obtaining a car title, it is worth paying attention to the possibility of purchasing electronic insurance. Since January 2017, all companies licensed for compulsory motor liability insurance are required to sell electronic policies. A complete list of such organizations with the addresses of their official Internet resources is available on the RSA website.

When issuing a policy electronically, the insurance company will not be able to refuse insurance or impose additional insurance. True, the electronic insurance system is still not fully debugged, so sometimes technical difficulties or software failures may arise. But if the website of one of the companies cannot cope with the load, the client is automatically redirected to the RSA website, where a replacement insurance company is selected for him, which can no longer refuse to sell the e-MTPL policy. This system is called “e-Garant”; it was created to ensure total availability of MTPL policies.

There is another option: use the OSAGO calculator, which allows you to calculate the price and issue a policy in one of the seven leading Russian insurance companies. The advantage of this method is the possibility of saving; not all insurance companies sell policies for the same price. Therefore, simultaneous payment in several organizations seems to be extremely beneficial in terms of saving time when searching for a car license with a minimum base tariff.

How to refuse imposed additional insurance when applying for compulsory motor liability insurance

When purchasing an MTPL policy not electronically, but in paper form, many car owners are faced with the problem of imposing additional services - such as the sale of voluntary insurance policies complete with a mandatory motor vehicle policy. Is it possible to avoid unwanted expenses, and how to refuse “voluntary-compulsory” insurance?

Once again, let us briefly outline the essence of the problem: when visiting the office of an insurance company or an insurance agent to conclude a compulsory motor liability insurance contract, car owners are often faced with the fact that they are refused to sell them a compulsory motor liability insurance policy without any additional insurance services - usually a voluntary life insurance policy. The insurance services imposed may vary, but the essence is the same: they are offered “in a package” with a car insurance policy, although this is illegal. If you find yourself in such a situation, you can act actively: make a video or audio recording of a conversation with the insurer, record the fact of refusal to sell a compulsory motor liability insurance policy without additional conditions and write a complaint to the Bank of Russia. However, if you want to save time and nerves, and at the same time leave with an MTPL policy on the same day, it’s easier to go the other way.

The simplest solution in this situation would be not to argue with the insurer, but to agree to take out voluntary insurance - and then, having received the MTPL policy, to immediately refuse the imposed insurance. This possibility is fixed in paragraph 1 of Bank of Russia Directive No. 3854-U.

When carrying out voluntary insurance (except for the cases of voluntary insurance provided for in paragraph 4 of this Instruction), the insurer must provide a condition for the return to the policyholder of the paid insurance premium in the manner established by this Instruction, in the event of the insurer's refusal from the voluntary insurance agreement within fourteen calendar days from the date its conclusion, regardless of the moment of payment of the insurance premium, in the absence of events in a given period that have signs of an insured event.

This is the so-called “cooling period”: it first appeared in 2015, and from January 1, 2018 it increased from 5 working days to 14 calendar days. It allows you to cancel unnecessary insurance within a specified period and return the money paid for it.

Having received the desired MTPL policy and an unwanted voluntary insurance policy in your hands, you just need to ask the insurer for an application form for refusal of the insurance contract , fill it out and attach to it copies of the necessary documents: passport (including registration), MTPL policy and title of the insured car, as well as a copy of the most unwanted policy. After the insurance company employee has accepted the documents, you need to receive your own copy of the application indicating the date the documents were received.

If an employee of an insurance company or an insurance agent for some reason cannot accept your application, you can do otherwise. The application form can be downloaded from the official website of the insurance company, filled out at home and sent to the insurer by registered mail with acknowledgment of receipt. The main thing is to keep the shipment within the same 14 days.

If we are talking about the standard set of tricks of insurers, then you can refuse almost all insurances imposed along with compulsory motor liability insurance: voluntary life insurance, property insurance, health insurance, all kinds of policies “against ticks”, “against the flu” and so on. Exceptions to the “cooling period” are specified in paragraph 4 of the same Bank of Russia Directive No. 3854-U: the opportunity to return money does not apply to medical insurance for traveling abroad, insurance for professional activities, medical insurance for citizens of other countries employed in Russia, as well as for international motor vehicle liability insurance policies (the so-called “Green Card”).

The amount of the refund depends on when the contract comes into effect - this needs to be clarified before signing it. If the policy has not yet entered into force before the cancellation, then the entire amount paid for it will be returned, and if it does, the insurer may retain part of the money for the few days that the policy was in force. It is better to clarify the terms of the policy in advance, but in any case the insurer will return most of the amount paid.

If your contract is included in the list of those that can be terminated according to the instructions of the Bank of Russia, and you submitted documents on refusal of insurance within the prescribed period (14 days), and the insurance company continues to refuse to return the money, you need to write a complaint to the Bank of Russia indicating all the details. The complaint can be sent by registered mail to the address 107016, Moscow, st. Neglinnaya, 12, or you can submit it electronically through the Internet reception, here.