Total loss of a vehicle under compulsory motor liability insurance

Total loss of a car under compulsory motor liability insurance: what is it, in what cases is it recognized, how is it calculated?

Civil liability insurance using a compulsory motor liability insurance policy provides for the obligation of insurance companies to pay damages to policyholders in the event of an insured event. The complete loss of a car, or, as it is often called, “total,” is one of these cases.

Total loss of a car is a situation in which it is not possible to repair the car or the repair will cost more than the market value of the car.

When is a car declared a total loss?

Complete, or constructive, loss of a car is recognized in cases where it is not possible to repair the damaged vehicle or the cost of such repairs is equal to or exceeds the market value of the car at the time of the accident (eighteenth paragraph of Article 12 of Federal Law No. 40 of April 25, 2002). It should be noted that most expert assessment systems of insurance companies recognize the total loss of a car even at 80% of the cost of repairs from the price of the car.

Calculation of payments upon the occurrence of total loss

Damage in the event of a complete loss of a car is defined as the value of the vehicle at the time of the insured event (that is, taking into account wear and tear at the time of the accident) minus the cost of the remaining usable parts (clause No. 4.12 of Bank of Russia Order No. 431-P dated September 19, 2014).

Dear readers! In our articles we consider typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , please contact us through the online consultant form on the right or call us at:

+7 (499) 110-33-98 Moscow, Moscow region

+7 (812) 407-22-74 St. Petersburg, Leningrad region

+7 (800) 600-36-17 Other regions

Online consultant >>

It's fast and for free !

The cost of property at the time of an insured event is the average price for such vehicles (market offers for the same brands, models, configurations, mileage, etc. are compared) on the secondary car market, which is calculated by insurance company specialists taking into account special coefficients.

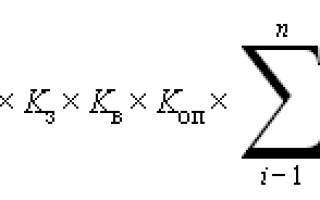

According to clause 5.5 of Bank of Russia Regulation No. 432-P dated September 19, 2014 “On a unified method for determining the amount of costs for restoration repairs in relation to a damaged vehicle,” the formula is used for calculations:

- C is the cost of the car before the accident;

- KZ is a coefficient that reflects the costs of work (disassembly, storage, etc.);

- KV - coefficient that reflects the period of use of the car before the insured event, as well as the average market demand for the remaining usable parts;

- KOP is a coefficient that reflects the degree of damage to the car;

- Ci is the percentage ratio of the cost of usable parts after an accident to the cost of the car before it;

- n is the number of remaining intact parts of the car.

A detailed description of the calculations is contained in paragraphs 5.6-5.9 of the above Regulations.

Useful residues after an accident

Useful parts, or remnants, are parts of the car that can be reused or sold.

There are no uniform rules for establishing the value of usable remains, which gives rise to controversial situations between the policyholder and the insurer. For obvious reasons, it is more profitable for insurance companies to inflate the cost of useful balances in order to reduce the insurance payment.

In accordance with clause 5.1 of Bank of Russia Regulation No. 432-P dated September 19, 2014, valid balances must meet the following requirements:

- must not contain damage that affects performance and presentation;

- there should be no design changes or parameters on the parts that were not originally provided by the manufacturer;

- There should be no traces of previous repairs on the parts.

Example: two cars were involved in an accident, one of them was damaged for 650,000 rubles, but the market value of this car, taking into account wear and tear, was 600,000 rubles. The cost of usable residues is 150,000 rubles, respectively, the amount of damage is 450,000 rubles (600,000 - 150,000). However, compensation under compulsory motor liability insurance will be only 400,000 rubles (Article No. 7 of Federal Law No. 40 of April 25, 2002), since this is the maximum amount for this type of insurance. The victim can demand the remaining 50,000 rubles directly from the person responsible for the accident in court.

How to apply for payment in case of total loss of a car

Since the car will be declared completely lost only as a result of an inspection by the insurance company, the algorithm of actions in this case does not differ from a standard road accident. You should contact the insurance company with an application, bringing with you the following documents:

- personal passport;

- PTS;

- certificate of accident;

- protocol on administrative or criminal offense;

- OSAGO policy;

- bank details where the funds will be transferred.

After this, the insurance company carries out all the necessary examinations and makes its decision. The policyholder can agree to this decision by signing the agreement, or they can prove that the amount is incorrect.

What to do if a controversial issue arises with the insurance company

The policyholder may have the following controversial situations with the insurance company:

- The Investigative Committee does not want to recognize the vehicle as dead;

- The Investigative Committee admitted the complete loss of the car, although this is not true (this happens much more often);

- Insurance company underestimates insurance payments;

- SK overestimates the cost of usable residues.

First of all, the policyholder who does not agree with the decision and calculations of the insurance company must carry out an independent examination (if the policyholder does not agree with the calculations for the usable balances, then two examinations are done).

The next step is to send a pre-trial claim to the insurance company, to which the following documents should be attached:

- copy of personal passport;

- copy of PTS;

- copy of the MTPL policy;

- results of independent examinations (should be done in triplicate);

- Bank details.

And if the conflict cannot be resolved amicably, then the policyholder has the right to file a claim in court. The following documents must be attached to the paper:

- copy of personal passport;

- copy of PTS and STS;

- copy of the MTPL policy;

- certificate of accident;

- protocol on administrative or criminal offense;

- results of independent examinations;

- Bank details.

Or ask a question to a lawyer on the website. It's fast and free!

Compulsory motor liability insurance contract after the total loss of the insured car

If a car receives such damage in an accident that its repair is impractical, it is considered that it is destroyed (or “total”). In this case, the insurance company pays the car owner monetary compensation (the amount of compensation under compulsory motor liability insurance or the full cost of transport with CASCO insurance, minus the cost of usable remains). At the same time, the complete destruction of a vehicle according to documents does not mean that it cannot be repaired and continue to be used. “Total” can be a beneficial situation for the car owner, provided that he takes into account all the legal nuances.

What happens to the insurance contract?

According to the rules of compulsory motor liability insurance, the contract is terminated early if the car is completely lost in an accident:

- the property in respect of which the insurance contract was concluded ceases to exist, which means the contract ceases to be valid, and the policy becomes invalid;

- the insurance company is obliged to reimburse the client for the cost of the policy for the unused period of validity.

Attention! After receiving an insurance payment for an accident, check your policy for validity on the RSA website or at the insurance company; there is a chance that your car was “totaled” and the policy was cancelled.

Is it possible to use the car after the “total”?

After the complete loss of a car or motorcycle, the MTPL policy (or its electronic version) remains with the car owner, but this does not mean that it continues to be valid. Lawyers of the Invest Consulting company do not recommend driving a vehicle restored after a “total” with canceled insurance:

- an invalid policy will not pass a document check by a traffic police inspector;

- after the start of monitoring of compulsory motor liability insurance by cameras (in Moscow, fixation systems are technically ready for this), fines will be issued automatically;

- If a driver with an invalid policy causes an accident, he will be required to compensate for the damage.

Legal assistance

By clicking the “Submit” button, you automatically agree to the processing of your personal data and accept the terms of the User Agreement.

What to do with a car after a complete loss?

Transport can “perish” only according to documents:

- old cars, the price of which is low, can be considered “lost” even with minor damage due to the high cost of spare parts. At the same time, their further use is quite possible;

- damage can only be external (body, optical elements, scratches on parts of a fallen motorcycle). They require minimal repairs and do not interfere with the continued use of the vehicle, but the insurance company may assess it as a total loss.

In these and other cases, if further use of the car or motorcycle is possible, the driver needs to take out a new OSAGO policy. It will most likely not be possible to register it with the same insurance company. You will have to contact another insurer. As long as the vehicle is not deregistered and can undergo technical inspection, a compulsory motor liability insurance policy can be issued for it. Participation in a total traffic accident in the past does not matter.

How to return part of the money for an MTPL policy after the total?

The procedure is not at all complicated, since in accordance with clause 1.13 of the MTPL rules, if the vehicle is destroyed, the contract is terminated early, and in accordance with clause 1.16 of the same rules, the insurer returns part of the premium for the unexpired period. The termination date is considered to be the next day after the accident in which your equipment received “total” damage, while the insurance company has 14 days from the date of receipt of notification from you to return your money.

Of course, ideally, the insurer should automatically return part of the money to you for the MTPL policy as soon as it terminates the insurance contract on the basis of “total”, but the point is that insurers are not the car owner’s best friend, so they terminate the policy, but They are in no hurry to return the money.

The legal department of "Invest Consulting" will help you in communicating with insurance companies; we have experienced lawyers.

What is the total under MTPL, how is the payment calculated and what do lawyers advise?

According to clause 16.1 of Art. 12 Federal Law No. 40 “On Compulsory Motor Liability Insurance”, the car owner has the right to receive financial compensation in the event of a complete loss of the vehicle. Among insurance organizations, it is customary to use the concept “total” to refer to such cases and make calculations taking into account certain features. What are the features of total MTPL payments and how is the calculation done?

What is total, total/constructive loss of a car?

The concept of “total” does not appear in insurance legislation, however, in practice it is used by insurers to designate an insured event that implies recognition of the absolute loss of the vehicle. The conditions for ascertaining the total are regulated by Federal Law No. 40 “On OSAGO”, where the relevant grounds are the impossibility of carrying out repair work due to the large amount of damage or the equivalence of the cost of the car and the costs of its restoration (clause 18 of article 12).

After determining the loss of the vehicle, the insurer undertakes to compensate the car owner for the market value of the car minus the surviving components. Various insurance companies, guided by internal policies, set their own damage coefficients, which serve as the basis for recognizing a vehicle as unusable. Typically they range from 60% to 85%.

Thus, a total insured event will mean the impossibility (total loss) or inexpediency of restoring the vehicle for economic reasons (constructive loss), which involves the payment of material compensation in accordance with the insurance contract and the legislation of the Russian Federation.

Conditions for recognizing the total loss of a car under compulsory motor liability insurance

With CASCO insurance, calculations of the threshold for a “total” insured event are tied to the market value of the car. In the case of compulsory motor liability insurance, according to clause 18 of Art. 12 Federal Law No. 40 “On OSAGO”, the complete loss of a car is established on one of two grounds:

- the cost of restoration work, according to the technical expert, is equal to or exceeds the market value of the vehicle at the time of the insured event;

- the amount of damage caused to the car is more than 60-85% of the total area.

Essential conditions when calculating for the insurer are the market value of the car at the time of the incident and the cost of repair work, including and excluding wear and tear. This is due to the fact that when recognizing the total, the formula uses the “market” value without taking into account depreciation, and when paying for restoration - taking it into account. Thus, after comparing the calculation results, the insurer interested in the minimum payment will choose the smallest indicator.

Additionally, the formula includes values that reflect the cost of surviving components. In this case, the amount of insurance payments cannot exceed the limit established by the legislation of the Russian Federation.

When is it beneficial for the insurer to recognize the constructive loss of a car under compulsory motor liability insurance?

In some cases, it will be beneficial for the insurance company to recognize the constructive loss of the vehicle, even if the amount of costs for restoration work does not exceed the cost of the vehicle. The insurer will take two factors into account:

- service life and year of manufacture of the car, since this indicator affects the actual cost on the market; the younger the car, the more expensive the surviving components, which will significantly reduce the amount of insurance payments;

- results of calculations of amounts payable, taking into account and excluding depreciation, in order to choose the smallest one.

Example. The insurer receives a car with a service life of 3 years at an average market price of 700 thousand rubles. Conditions and calculation:

- the market value of the car at the time of the insured event is 620 thousand rubles;

- the cost of repairs taking into account wear and tear is 400 thousand rubles;

- cost of repairs excluding wear and tear - 600 thousand rubles;

- the cost of usable remains is 300 thousand rubles.

Thus, for payment with recognition of the total: 620,000 - 300,000 = 320,000; payable without total recognition: 400,000 (cost of repairs excluding wear and tear). In this case, it is more profitable for the insurer to recognize the total and pay 320 thousand instead of 400 thousand.

In cases where the cost of repairs is higher than the value of the car, but it is not profitable for the insurer to pay the total insured amount, companies resort to various methods of falsifying expert assessments, so the policyholder often prefers to turn to independent organizations for help. By providing a document indicating real values, it is easier to avoid fraud on the part of the insurer.

How is the payout amount calculated? Details with example

When calculating insurance payments, the recommendations “On a unified methodology for determining the amount of expenses” established by the Central Bank of the Russian Federation are used. If the vehicle is recognized as a complete loss, the amount payable is calculated using the formula SSV = RSA - SGO, where:

- TIC - the amount of insurance payments payable in connection with the destruction of the vehicle;

- RSA - the market value of the car before the transport accident leading to the loss of property;

- SGO - the cost of usable remains or surviving components that are subject to further use.

Example. The insurer received a car with a service life of 5 years. At the time of acquisition, its cost was 800 thousand rubles, and at the time of calculation it averaged 720 thousand rubles on the market. The total cost of usable remains in the car amounted to 250 thousand rubles. Calculation: 720,000 - 250,000 = 470,000. However, the insured is subject to payment of 400 thousand, and not 470 thousand on the basis of Art. 7 of the Law “On Compulsory Motor Liability Insurance”.

As of 2019, according to Art. 7 clause b) of Federal Law No. 40, the insurer undertakes to reimburse the policyholder for expenses for loss of property not exceeding 400 thousand rubles. The car is not subject to mandatory disposal after payments, but is returned to the owner along with the surviving components or remains with the insurer.

Underestimation of the amount of payments by the insurance company: when and why

Insurance organizations often include clauses in the contract with the policyholder regarding the conditions for the subsequent operation of the vehicle after recognition of a total loss. For example, the amount of insurance payments in the event that the car is returned to the owner will be significantly lower than when it is transferred to the insurer, since the equivalent of depreciation and the cost of usable remains are calculated from the amount. In this case, it is more profitable for the insurance organization to recognize the complete loss of the car with its subsequent sale.

It turns out that it is more profitable for the car owner to obtain insurance for the repair of a car that was subject to restoration, however, the insurer recognizes the loss of the vehicle with its subsequent seizure, which is most appropriate for the owner, and then sells a fully functional car through partners, receiving additional profit.

In addition, according to clause 1.13 of the law “On Compulsory Motor Liability Insurance”, after making payments for the loss of a vehicle, the insurer ceases interaction with the policyholder, and the contract ceases to be valid. This is undoubtedly beneficial to insurance organizations, since a car with significant damage will increasingly lead to situations requiring insurance payments.

Also, in order to underestimate the amount of payments, insurers often recognize surviving components as unfit for use or maneuver with estimates of market value.

Calculation and features for total insurance according to compulsory motor liability insurance if the car is old

Insurers often resort to various manipulations with assessments if they receive an old car. This happens for the following reasons:

- the older the car, the lower its market price, which increases the likelihood of increased repair costs in relation to the value of the car;

- the cost of usable balances on old-generation cars will be significantly lower, which will lead to an increase in the final amount of payments;

- an old car has a high insurance risk.

It will be enough for the insurance organization to simply set the total, even by slightly underestimating the market value of the car. In this case, the amount to be paid will be several times lower, and the organization will terminate the contract with the unprofitable policyholder.

When receiving insurance payments for an old car with a large percentage of damage, it is recommended to contact independent experts to reduce the likelihood of falsification of information used in the calculation.

Calculation and features for total insurance according to compulsory motor liability insurance, if there are suitable parts left

According to the explanations in paragraph 54 of Plenum Resolution No. 58, the insurer cannot return the usable remains to the owner of the car against his will. Thus, the policyholder has the right to either pick up the components or leave them with the insurer. In this case, the cost of the parts must be reimbursed together with the total payment amount. However, it is not profitable for the car owner to keep the components for a number of reasons:

- you need to independently look for a buyer to sell components that are not used;

- the amount of insurance payments is significantly reduced, since the amount will be calculated taking into account depreciation;

- the policyholder will bear the costs of terminating the registration of components with the State Traffic Inspectorate.

According to paragraph 18 of Art. 12 Federal Law No. 40, the total amount of insurance payments is the cost of the car at the time of the insured event minus the surviving components. If you leave the balance to the insurer, the policyholder will be reimbursed for the cost of the car, but not more than 400 thousand rubles.

Lawyer's advice: is it profitable to receive a total payment?

It is beneficial to receive total payments if the value of the car before the incident was not high, and there are few surviving parts left. For example, if the price of a car is 400 thousand, and there are 50 thousand remaining balances, then OSAGO will offer about 250-300 thousand for payment, which is a significant percentage of the market value of the vehicle.

At the same time, payments for the destruction of expensive cars with a small amount of residue will not be beneficial to the policyholder, but will be quite beneficial to the insurer if the car remains with him. In this case, it is better to try to prove the possibility of restoring the vehicle in court. It is necessary to rely on the list and value of surviving remains, making a complete list of them in the calculations.

Thus, if the car received a large percentage of damage or its value is lower than the cost of restoration, then there is a high probability of calculating insurance payments on the total. Insurance companies often resort to manipulation with calculations in order to reduce the amount of payments, so it is recommended to calculate compensation yourself or contact independent experts.

Total loss of the car under OSAGO and CASCO

🔔 A private auto lawyer will save your money. 🔥 100% guarantee, payment upon delivery. ☎ tel: +7 495 290-92-46.

Contents of the article (click for quick access) :

As a result of an accident, the car may receive such damage that will lead to its complete destruction. In accordance with Article 18 of the Federal Law of April 25, 2002 “On compulsory civil liability insurance of vehicle owners” No. 40-FZ, this term should be understood as damage as a result of which the car cannot be restored or the cost of repairs exceeds the actual price of the car before the accident. As for voluntary insurance, the number of insured events that can lead to total (constructive) death is somewhat greater.

Total for “automobile citizenship”: main features

The conclusion about the complete loss of the vehicle under compulsory motor liability insurance is made after an examination and determination of the total amount of repairs necessary to eliminate the damage. We can talk about constructive loss when the cost of restoring a car reaches 65-80% of its market value. In such a situation, appraising technicians determine the value of the components, assemblies and structural parts that survived the collision. These elements suitable for further use are called usable residues. Their price is determined using a universal method. In doing so, take into account:

- the value of the car in undamaged condition;

- “age” of the car and period of operation before the incident;

- total number of damages;

- costs associated with the removal, storage and pre-sale preparation of spare parts;

- percentage ratio of undamaged elements to the cost of the car.

Having determined the value of usable remains, specialists begin to determine the extent of general damage to the machine.

Payment of compensation under compulsory motor liability insurance

The owner of a vehicle involved in an accident is obliged to submit a claim to the insurance company within 5 working days after the accident. The law obliges the insurer to consider the appeal within 20 working days. After this period, he must:

- transfer funds;

- issue a referral for repairs;

- refuse to pay compensation.

The refusal must be reasoned and sent to the policyholder in writing. Violation of the deadline for consideration of the application or leaving it unattended gives the owner of the car the right to demand not only compensation for damage, but also payment of a penalty in the amount of 1% of the insured amount.

In case of complete constructive loss of the car, the amount of compensation must correspond to the market value of the car on the date of the accident minus the price of the usable remains. We must not forget about the maximum amount of payment established by law for “motor vehicle insurance,” which currently amounts to 400 thousand rubles (material damage). If the cost of restoring the car exceeds this amount, then the remaining funds are recovered from the person responsible for the incident. The driver whose actions led to the collision has the opportunity to comply voluntarily. Otherwise, the victim has the right to seek compensation in court.

Total loss under CASCO

The CASCO agreement, unlike the “automobile insurance” agreement, provides for compensation for losses in the event of total loss of the car, not only as a result of an accident, but also in the event of a number of other insured events. It could be:

- hijacking;

- drowning;

- vandalism;

- arson;

- accidental damage to equipment due to the fault of the owner;

- other incidents that led to the impossibility of restoring equipment.

The amount of payment for voluntary insurance depends on the amount for which the car was insured. Comparing compulsory and voluntary insurance contracts for the total loss of a vehicle, we can conclude that the difference between them is:

- payment method;

- exchange of compensation;

- procedure for interaction between the parties.

As practice shows, total under CASCO occurs when 65-75% of damage is received.

CASCO: how car owners can receive payment

The procedure for paying compensation in the event of a total loss of a car under CASCO differs from the one that insurers have to go through under “automobile insurance.” The most important difference is the size of the insurance premium and mandatory accounting for depreciation, which increases by an average of 1% monthly. The legislation of the Russian Federation provides for two options for payment in case of total loss of a car under CASCO:

- Insurance pays in full minus depreciation. The owner relinquishes ownership. The vehicle becomes the property of the insurance company.

- Ownership rights are retained, and the total amount of payment is determined taking into account the depreciation of the machine and the value of the usable remains.

The right to choose a convenient option remains with the car owner. The decision is made taking into account the release date of the equipment, the nature of its operation, performance qualities and a number of other features.

We can help!

Below are some of the cases won with supporting documents. We are guaranteed to help you in the fight against dishonest insurers. Payment is made only after the fact and only if the outcome of the case is positive.

Collected in court

Collected in court

SK Opora

SK Angara

Collected in court

Collected in court

Owners of used cars and cars on credit

Automotive lawyers are often asked whether the total loss of a car is compensated under CASCO for used cars. This is an important point, since insurance is quite expensive and car owners should know what to expect if a serious problem occurs. In practice, such situations rarely arise. Insurance companies refuse to enter into contracts with car owners whose property is more than 7 years old.

The situation is completely different if the car was insured under MTPL. After the insurance company receives a statement about the occurrence of an insured event, an independent examination will be carried out. The car owner must be prepared for the fact that the assessment will be minimal. Appraiser technicians working with the insurer will definitely take into account the cost of the surviving elements, and the insurance company will deduct them from the insurance payment. As practice shows, the funds received are not enough to restore equipment or purchase a new (even used) car.

We previously said that when selling a vehicle on credit or leasing, the selling company insists on issuing a CASCO policy. In case of constructive loss of the car, the bank becomes the beneficiary. In this case, the compensation received will be used to repay the bank loan. If the payment amount exceeds the balance of the debt to the banking organization, the remaining funds are transferred to the driver. It is important to remember that in this case the loan agreement is closed, and the person who purchased the vehicle in this way is left without a car.

Receiving payment: procedure and list of required documents

In order to receive the required payment from the insurer, the applicant must provide a package of documents. It consists not only of a statement, but also:

- insurance policy;

- ID cards (usually a civil passport is used);

- driver's license;

- papers confirming ownership of the vehicle;

- receipts confirming payment for tow truck services, parking and other expenses.

If not all the papers were presented to the insurer, it may postpone consideration of the application, but this is not a reason to refuse compensation for damage.

If involved in an accident on the road, the car owner must follow the procedure established by the traffic rules. Next he:

- reports the incident to the insurance company (the contract may provide for calling a representative of the insurance company to the scene of the incident);

- call traffic police inspectors (accidents in which damage exceeds 100 thousand rubles, and in some cases 400 thousand, cannot be registered independently;

- prepares an application for compensation of losses and a package of documents confirming the right to receive compensation;

- presents the vehicle for inspection, signs the specialist’s conclusion or does not agree with it.

An application for the occurrence of an insured event under MTPL and supporting documents is submitted to the insurance company within 5 business days after the collision. The insurer has 20 days to review it and make a decision. As for voluntary insurance, the period during which it is necessary to apply to the insurance company is stipulated by the contract. The agreement also specifies the period for reviewing the CASCO application and making payments.

Compliance with deadlines must be treated with special attention, since their violation without a good reason may become grounds for refusal to compensate for losses.

Conclusion

The complete loss of a car is a serious problem for its owner. Insurance companies are reluctant to part with large sums, so the car owner must be prepared for a serious and lengthy fight for his rights. An auto lawyer will help you cope with this difficult task. The lawyer will provide a free initial consultation and represent the client’s interests in all authorities and authorities.

What is total loss of a car under compulsory motor liability insurance?

After an accident, not surprisingly, the cars are left in a very damaged condition. The insurance company can determine the total loss of the car under compulsory motor liability insurance (otherwise known as total) with damage ranging from 65 to 80%. According to OSAGO, a car is considered “lost” if the cost of repairs is equal to or greater than the price of the vehicle at the time of the insured event.

For example, before the accident, your car (taking into account the fact that it was in use) cost 300 thousand rubles. Repairing it after an accident will require 350 thousand rubles. This means that we can assume that the car cannot be restored, this is its complete destruction. In this case, the insurance company will pay you the value of the car before the accident, reduced by the price of the spare parts remaining suitable for further use. That is, if suitable spare parts cost 30 thousand rubles, then you will receive 300 thousand - 30 thousand rubles. = 270 thousand rubles. It turns out that it is in the interests of the insurance company to significantly reduce the insurance amount; for this they inflate the cost of the remaining spare parts.

Another way to solve the problem is to transfer the lost car to the insurance company and receive the full insurance amount. When it comes to an expensive car, the situation is different. The full insurance amount for compulsory motor liability insurance is 400 thousand rubles. (for all). In this case, if the car cost 900 thousand rubles, its repair after an accident will cost 930 thousand rubles, and the price of suitable spare parts is 300 thousand rubles (900,000 - 300,000 = 600,000), then the insurance company will, at best, pay only 400 thousand roubles. instead of the expected 600 thousand, and the remaining amount will have to be recovered from the culprit of the accident through the court.

Important : after a fire there are practically no usable spare parts left; the insurance company pays the insured amount in full at the cost of the car at the time of the insured event.

Total loss of the car under compulsory motor liability insurance

Methods for recognizing the death of a car are regulated using the Unified Methodology approved by the Bank of the Russian Federation. A conclusion about the loss of a vehicle can be issued by an expert technician who assesses the amount of damage to property and signs the expert report. He works in the interests of the insurance company, so his conclusions may not entirely correspond to reality.

If the owner does not agree with the decision to completely destroy his car, then he has the right:

- provide evidence to the court about the real possibility of restoring the car;

- conduct an independent expert assessment, and, if the experts’ conclusions do not coincide, demand compensation for the difference in assessments through the court;

- in the event of a complete loss of the car, demand an accurate market valuation of the remaining usable spare parts;

- Having an agreement with OSAGO in hand, it is better to renounce the property rights to your car in favor of the insurer.

Complete technical loss of a car occurs if its repair without taking into account wear and tear is more expensive than or equal to its market price at the time of the emergency. The market value of a new car is easy to determine - receipts and contracts will serve as evidence. The cost of repairing an old vehicle will probably exceed its market price at the time of the accident, and suitable spare parts, taking into account their wear and tear, do not have a high value at all. The interests of the insurer in this option lie in significantly understating the market price of the car.

How is compulsory motor liability insurance paid if the car is completely lost?

According to the rules approved by the legislation of the Russian Federation, the amount of insurance payments for a lost car must correspond to the full cost of the vehicle at the time of the situation. No deductions are provided from this amount, however, insurers try by all means to underestimate the amount of payments to the policyholder. That is why an independent examination is necessary.

Note: in many cases, the client receives an amount that will not be enough to repay the debt on the car loan. The insurer then receives a car that it can restore and sell.

Payment of insurance compensation depends on the decision of the policyholder. It has two different solutions:

- Receive the full insured amount by placing your lost car at the disposal of the insurer.

- Receive the insured amount minus the depreciation of the car and the price of suitable spare parts, leaving the damaged car in your property.

The maximum amount of insurance compensation is 400 thousand rubles, and this amount does not include the wear and tear of the car or the cost of its repair. The policyholder can give his wrecked car to the insurer without his approval. According to the new law on compulsory motor liability insurance, insurance compensation can be replaced by car repairs, during which the company saves by using used parts. This is illegal and can only happen with the written permission of the victim.

Repairing a car after an accident requires the purchase of spare parts and consumables, as well as payment for the services of mechanics, a tow truck, and for storing the vehicle until it is inspected and examined. The price of consumables and paint coatings is also taken into account. Sometimes an expert recognizes the damage as not related to a given accident, so the cost of this part is not included in the insured amount. If a person was injured in an accident, moral damages may also be recovered.

Manufacturers set standards for all work carried out in car service centers, calculated in standard hours. The cost of work is determined by multiplying the cost of a standard hour by the time of a standard operation. This way you can calculate how much mechanic services will cost.

To receive the full amount of damage under the insurance policy, you must write a statement and hand it personally to the insurer. Make a copy of this statement. On it, the company employee must put a note indicating the date of receipt of the application and put his signature.

When is it profitable for an insurer to recognize a constructive loss of a vehicle?

Due to the significant number of foreign cars on our roads, prices for spare parts for them have increased, and, accordingly, losses in an emergency situation have increased. Depending on their interests, insurance companies increase or decrease the cost of spare parts and repairs in order to create a semblance of car destruction. For example, it is beneficial for the insurer to recognize an almost new car with minor damage as lost, because in this case the client can refuse the car in favor of the insurance company, thanks to which they significantly underestimate insurance payments. The lack of approved methods for calculating the value of a car in a pre-accident condition and the possibility of accurately calculating the value of remaining usable spare parts plays into the hands of insurance companies.

If you are sure that the insurance company is deliberately underestimating the amount of money paid, then you should contact experienced lawyers who will tell you what to do in this situation. A prerequisite will be the involvement of independent experts in resolving this controversial issue.

It is especially beneficial for insurance companies to recognize the constructive loss of almost new cars. Spare parts for them are very expensive, and payments are made according to the following scheme: market value minus the cost of suitable spare parts. The only exception may be completely new cars, for the purchase of which there are receipts and contracts.

All actions of the insurance company have certain regulations. The insurer may significantly delay the moment of the final decision, citing additional examinations or delaying the work of the car service to clarify the diagnosis of damage. The insurance company may offer to conclude additional agreements on the sale of a salvage car to third parties, but you cannot agree to this, since you will have nothing to show in court - you yourself agreed!

If there are any usable car parts left

Useful car parts after an accident are spare parts and assemblies that you can use to repair another similar car or sell. As already mentioned, the policyholder has the right to completely refuse them in favor of the insurer, or to keep them for himself. Insurers try in various ways to inflate the value of these balances in order to significantly reduce the amount of insurance payments. All possible methods are used:

- selling the remaining spare parts through an auction, where a figurehead specifically increases the cost of each lot;

- recognizes as suitable those units that cannot be restored;

- sets obviously inflated prices for the remaining parts and components.

Insurance compensation is significantly reduced and you will no longer be able to purchase a similar car. To avoid getting into such a situation, you should contact a specialist - an expert who will determine the suitability of each part, unit and assembly, as well as their market value at the time of the accident.

As a last resort, you can sell the remainder of your car yourself. Resellers buy damaged cars well. Another way out of the situation is to use the salvage vehicle as a donor for another similar vehicle.

Useful video

Below you can see more about the car's restoration.

Conclusion

A car after an accident requires a thorough inspection by an independent expert. If your vehicle is deemed unrepairable (or a total loss), you are entitled to full compensation for its value at the time of the accident. When signing the contract, pay special attention to whether the percentage of damage at which the car is considered lost is not underestimated. Carefully study all clauses of the contract, especially those related to possible payments. If there is anything you don't understand, ask for clarification.

If your car can be repaired for 30-50% of its cost, it makes sense to get the cost of the remaining parts under the MTPL policy. The calculation of the amount of the insured's losses is not approved by law.

It is in the interests of the insurer to minimize payments for compensation for its damage. To do this, they use all available methods. Be prepared to make a serious decision - whether to give your vehicle to the insurance company or not, the amount of payments due to you also depends on this.

Court cases on such issues are resolved quickly and mainly in favor of the policyholder. In this case, the insurer pays all legal costs and the amount of payments assigned by the court under the policy.